JPMorgan, IMF, World Bank and payment giants send mixed signals on a global recession. Watch these signs, data and expert forecasts for 2025.

Why does a recession happen, and how can you see it coming?

In 2025, global headlines from JPMorgan, the IMF, the World Bank and payment giants like Visa and Mastercard paint a mixed picture.Consumers keep spending. Jobs remain surprisingly strong. Yet key red flags — from yield curve inversions to weak manufacturing data — warn that an economic slowdown could be near.

A recession is a significant decline in economic activity spread across the economy, lasting more than a few months. Key triggers include:

- Falling consumer spending (the biggest driver of GDP).

- Rising unemployment, layoffs and business closures.

- Declining industrial output and business investment.

- Weakening global trade and supply chains.

A Slowdown but Not a Crisis — Yet

The global economy in 2025 finds itself at a crossroads, balancing solid momentum with clear indicators of a slowdown. JPMorgan Chase, for instance, has adjusted its estimated probability of a U.S. recession this year to 40%, a notable decrease from its earlier estimate of 60%. This revised outlook is largely attributed to continued robust consumer spending and strong labor markets within the United States.

However, a more cautious tone comes from international financial institutions. Both the International Monetary Fund (IMF) and the World Bank have issued warnings about persistent inflation, elevated borrowing costs, and the potential impact of new tariffs. These factors, they suggest, could easily push global economic growth into negative territory should further shocks occur.

“While recent data suggest resilient activity, we see clear downside risks, mainly from trade tensions and stubborn price pressures,” stated Pierre-Olivier Gourinchas, the IMF’s chief economist. In its April World Economic Outlook, the IMF projected global GDP growth at 3.2% for 2025. While this figure indicates moderate growth, it’s important to note that it’s significantly higher than the 2.5% pace discussed in earlier forecasts, which would have marked the slowest mid-decade growth since the 2008 financial crisis.

Mixed Signals from Banks, Card Networks, and Central Banks

The World Bank’s June 2025 Global Economic Prospects report paints a similar picture: global growth has slowed to an expected 2.3% this year, dragged down by fragile investment and weaker goods trade. Advanced economies led by the U.S. and Europe are expected to grow just 1.3–1.5% on average.At the same time, payment giants Visa and Mastercard continue to post upbeat earnings.

Visa, which reported its Q2 FY25 results in late April 2025, showed global payments volume rose 9% year-over-year. Mastercard, whose Q2 FY25 earnings are anticipated to be released on July 31, 2025, is widely expected to report strong revenue growth, with speculation of a climb around 14%. These figures, once fully confirmed, would suggest that, so far, households are still spending, though Mastercard had previously flagged early signs of softness in discretionary travel and cross-border purchases.

Labor Market Soft Spots: Early Cracks in a Strong Jobs Story

One reason recession calls remain cautious is the continuing strength of the labor market but the edges are fraying in some regions. In the UK, new data this week from the Office for National Statistics (ONS) showed unemployment rising to 4.7% for the March-May 2025 period, the highest since mid-2021. Total payrolls have dropped by 178,000 year-on-year, based on early estimates for June 2025 payrolls — a clear reversal from last year’s tight labor squeeze.

In Australia, unemployment climbed to 4.3% in June 2025, up from 4.1% in May, enough to fuel calls for the Reserve Bank of Australia (RBA) to slash interest rates to head off a deeper slowdown. Yet the RBA has so far held steady, citing underlying inflation risks.

In the United States, jobless claims are still low by historical standards, initial claims fell by 7,000 to 221,000 last week (for the week ending July 12, 2025), according to the U.S. Labor Department. The unemployment rate for June 2025 sits at 4.1%, just above last year’s 3.7% floor. The so-called Sahm Rule, a rule of thumb that flags recessions when the three-month average unemployment rate rises by at least 0.5 percentage points above its low, is not yet triggered.

Tariffs Back in Focus: JPMorgan’s Stagflation Warning

One factor weighing heavily on forecasts is the resurgence of tariffs. JPMorgan strategists warned in late June that rising trade barriers — including new U.S. tariffs on Chinese tech imports and the EU’s carbon border adjustment mechanism — could push prices up while slowing demand, creating conditions for stagflation (stagnant growth + high inflation).“Tariff escalation remains a critical downside risk,” JPMorgan’s global chief economist Bruce Kasman said. The bank’s base case: U.S. GDP growth at just 1.3% this year, with an “uncomfortable risk” that policy errors or shocks tip it below zero.

Visa, Mastercard: Consumers Still Spending — But Cautiously

One bright spot is that households are not pulling back sharply yet. Visa’s Spending Momentum Index (SMI) shows daily spend is above the 100 baseline, meaning more consumers are spending more than they were a year ago. Retail, travel, and entertainment are all still seeing robust transaction volumes.

Mastercard’s anticipated Q2 earnings would likely echo this. The company is expected to report gross dollar volume in the range of $2.3 trillion last quarter, with an estimated 14% year-over-year increase, but cross-border travel spending has started to cool — a signal that consumers are becoming selective about discretionary trips.

Rising debt burdens are the hidden risk. U.S. credit card balances hit $1.18 trillion in Q1 2025, according to the New York Fed, with Q2 figures expected to be released soon and speculation that they might approach $1.3 trillion. Delinquency rates have edged up to 3.05% in Q1 2025 — still low by historical standards but rising from pandemic-era lows.

Markets Are Watching the Yield Curve — And So Should You

Financial markets are sending mixed signals too. The yield curve — a classic recession harbinger — has been a point of focus. On July 17, 2025, the yield on 2-year U.S. Treasury notes hovered around 3.92%, slightly below the 10-year yield at 4.46%. While inversions have historically preceded U.S. recessions, the curve was not inverted on this specific date.However, strong jobs data and resilient consumer spending have so far delayed that gloomy outcome. The Conference Board’s Leading Economic Index — another recession gauge — has declined for an extended period, leading to concern among many analysts.

Housing and Manufacturing: Weak Links to Monitor

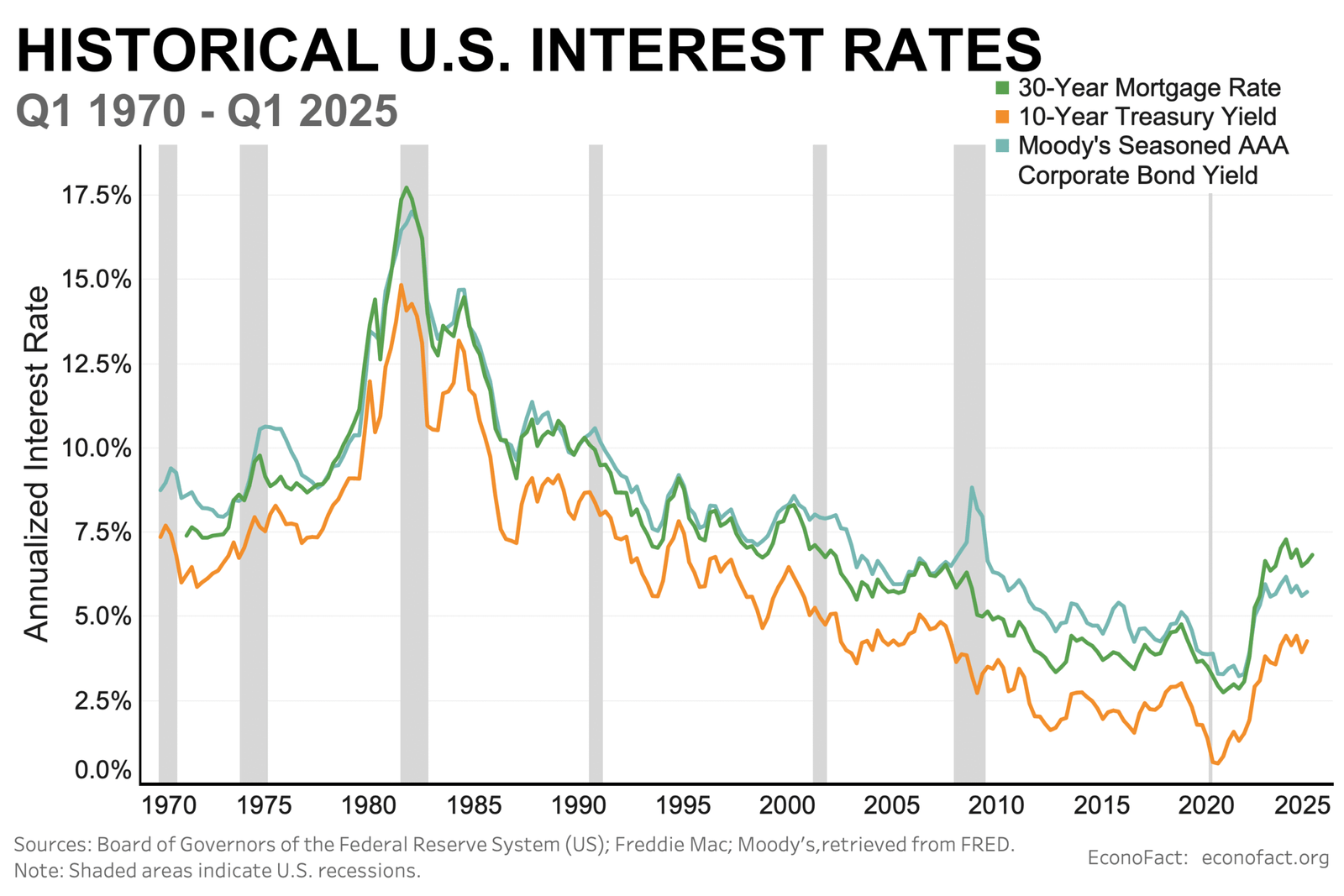

Housing is another piece of the puzzle. According to Redfin, while U.S. median home prices generally continue to rise at a slower pace nationally, some high-cost cities have seen modest year-over-year declines or flat growth during Q2 2025. Mortgage demand remains depressed, as the average 30-year fixed mortgage rate sticks around 6.75-7% — near two-decade highs.

Construction hiring has seen mixed signals; the Associated General Contractors of America reported that construction employment increased by 15,000 jobs in June.

However, fewer new projects in certain segments could still be a drag on GDP growth if the trend continues.

In manufacturing, Volvo Trucks reported this week that North American truck deliveries in Q2 2025 declined by 20%, with orders also declining by 16% year-over-year — a stark sign that businesses may expect weaker freight demand. Freight and trucking are classic early-cycle indicators, often cooling before broader contractions appear in official GDP numbers.

ALSO READ: Earth’s Rotation Accelerating, Scientists Warn of Shorter Days and Time Corrections

Central Banks: Torn Between Rate Cuts and Inflation

Policy responses remain a balancing act. The U.S. Federal Reserve has maintained its federal funds effective rate around 4.33% through June 2025, signaling it may not cut rates until late 2025 if inflation stays sticky. June’s U.S. inflation (CPI) print came in at 2.7%, still above the Fed’s 2% target.In Europe, the European Central Bank (ECB) delivered its first rate cut in June but is treading carefully after core inflation for June 2025 remained at 2.3%, just above their 2% target.In Australia and the UK, policymakers face conflicting pressures: weakening labor markets demand relief, but high services inflation holds them back from aggressive easing.

So, are we headed for a repeat of 2008?

Probably not — at least for now.

Soft Landing

Many banks, including JPMorgan and Goldman Sachs, still believe a soft landing is possible: growth slows but doesn’t contract, labor markets soften gently, and inflation comes down enough for central banks to cut rates by early 2026.

Stagflation Risk

The risk that worries forecasters is stagflation. Tariffs could keep prices high even as growth weakens — the worst of both worlds for policymakers. JPMorgan’s base scenario leans toward mild stagflation rather than deep contraction.

Mild Recession

A mild, short recession can’t be ruled out if job losses accelerate or consumers close their wallets. A shock like a major supply chain disruption or financial stress event could quickly turn forecasts darker indicating recession risk.

What Should Households and Businesses Do Now?

Economists say that for now, the best defense is vigilance and financial prudence.

For households:

- Build or maintain an emergency fund covering 3–6 months of expenses.

- Avoid new high-interest debt if possible.

- Keep spending in check, especially for big-ticket discretionary items.

For businesses:

- Strengthen cash reserves.

- Consider locking in borrowing costs if rates soften.

- Diversify suppliers to reduce tariff or geopolitical exposure.

Bottom Line: Stay Alert but Don’t Panic

The economy’s big engine — consumer spending — is still running. But the warning lights are blinking: higher unemployment in parts of Europe and Australia, a closely watched yield curve (though not currently inverted), softening housing and freight, and the specter of more tariffs.

For now, the probability of an outright global recession remains under 50% — but the risks are too real to ignore.

As IMF managing director Kristalina Georgieva put it in a recent panel: “We are not headed for a crisis, but complacency is the biggest risk. The world must watch the signs — and be ready to act.”

Key Sources

JPMorgan Global Markets Outlook, June 2025

World Bank Global Economic Prospects, June 2025

Visa Fiscal Second Quarter 2025 Earnings Release

Mastercard Q2 FY25 Earnings Call Schedule (July 31, 2025)

ONS UK Labour Market Bulletin, July 2025

ABS Australia Jobs Data, July 2025

U.S. Labor Department, Initial Jobless Claims, July 2025